What are the best businesses to own?

In a 2014 interview, Carol Loomis, Warren Buffett’s de facto editor in chief, asked him, what is a good business.

A good business is the one that earns a high rate of return on tangible assets. That's pretty simple... The very best businesses are the ones that earn a high rate of return on tangible assets and grow.

How can you not love Warren Buffett? Like his late business partner Charlie Munger, he often distills decades of experience, knowledge and wisdom into short, memorable, golden nuggets of truth.

Still, the danger to you and to me, those of us seeking wisdom and guidance as we make our own way in the world of investing, is that we take the Oracle’s words at face value without bothering to consider whether we understand his true meaning.

The very best businesses are the ones that earn a high rate of return on tangible assets and grow.

Seems intuitive enough, but let’s make return on tangible assets less abstract and more…tangible. (These are the jokes, people)

Tangible assets

Tangible assets refer to assets that are physical and measurable that the company uses to operate. Think inventory, furniture, property, buildings, etc., as well as securities like cash, stocks and bonds. Basically, if it can be counted and it has a market value, it's tangible.

Contrast those with intangible assets: patents, trademarks, etc. These matter, sometimes a lot, but since they're difficult if not impossible to put a price on, and you can't hold them in your hand, they're intangible. Since you can't reliably value them, calculating a 'return' on these assets is rather pointless.

High rate of return

Typically, though not always, return refers to the Net Income generated in a given period. So...

Return on Tangible Assets (ROTA) = Net Income / Tangible Assets

Let's look at a simple illustration.

Say Arthur's Bakery is the best bakery in town. It has one location filled with all of the necessary equipment, ingredients and inventory necessary to dominate the local baked goods scene.

Arthur, the owner, keeps clean books and has a record of all of his assets, both current (e.g., cash on hand, boxes, flour, etc.) and fixed (e.g., equipment, delivery truck).

Mort, an ambitious and enterprising relative of Arthur's, wants to open his own bakery. Arthur, being the generous man he is, tells Mort everything he needs to know, including what he needs (assets) to run the business.

Before long Mort has a bakery open in the same shopping center. He's copied Arthur's operation down to the line item.

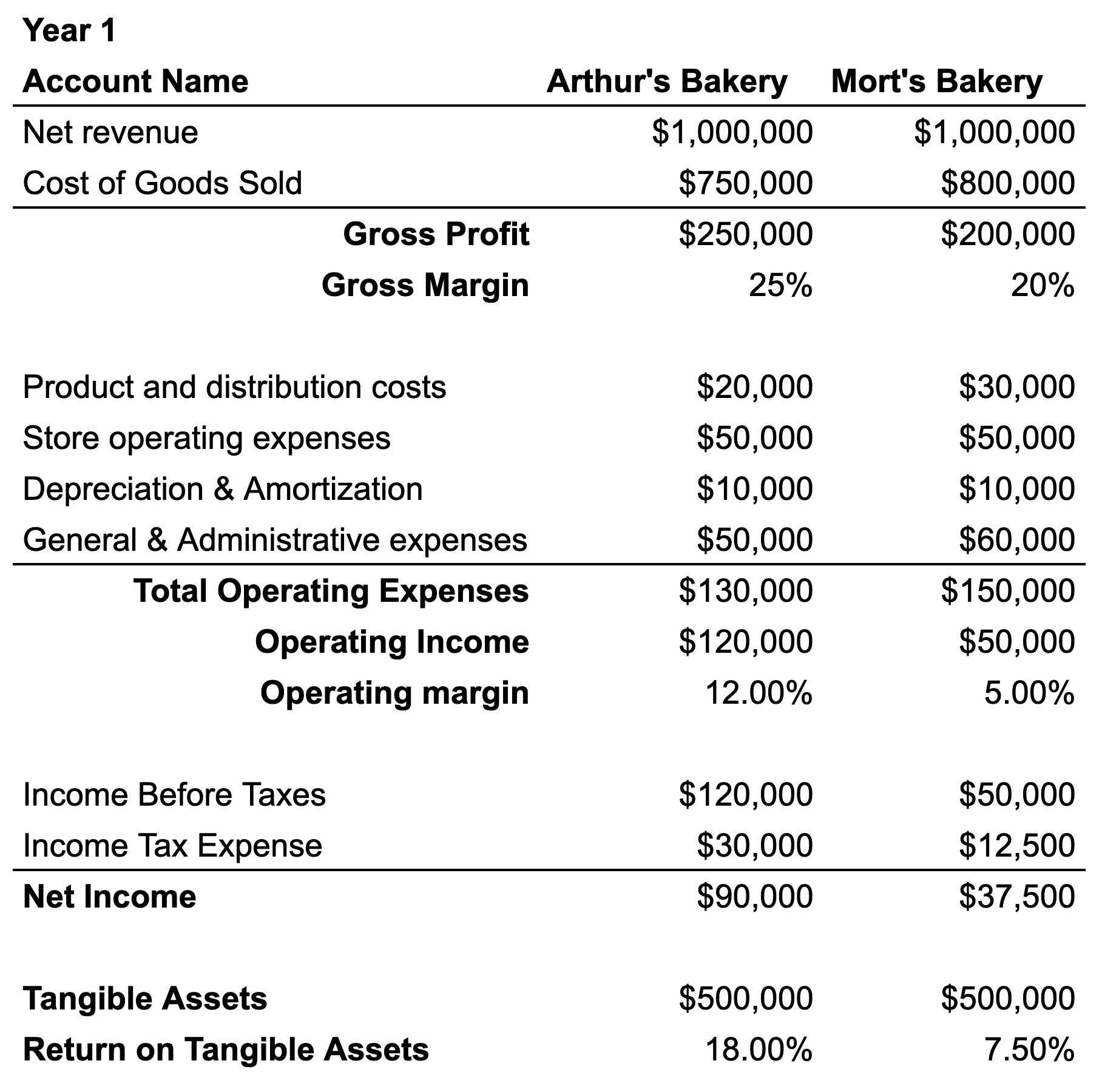

Arthur and Mort have the same Tangible Assets, each carrying a total value of $500,000 on the books.

Mort proves to be a terrible baker. He burns his buns, chars his cookies, and routinely puts salt in where the recipe calls for sugar. Because of this, his products aren't exactly in high demand so he prices every item in his shop for $1 less than whatever Arthur is charging.

Mort hustles. He manages to generate the same amount of net revenue that Arthur's bakery generated last year.

It's a respectable outcome, but he has issues managing his operating costs. And since he was starting from scratch (now that's a baking joke) his suppliers aren't offering him any volume discounts, so his gross profit - what's left after he subtracts the cost of the goods he's sold - isn't as strong.

In short, despite Mort having Arthur's playbook, and despite matching Arthur's total revenue, his business isn't as good as Arthur's.

Let's look at the financials.

Warren Buffett says a good business is one with high Return on Tangible Assets. Why?

Well, think about what a high Return on Tangible Assets reveals about the business and its management's skill. Consider our fictitious (delicious) example:

- Arthur's reputation with his vendors led to a higher gross margin.

- Arthur's reputation with his customers meant that his product and distribution costs were lower. He sells a premium product, so he doesn't need the volume that Mort needed.

- Thanks to strong operating discipline, Arthur was also able to keep his General & Administrative expenses in check.

- Despite Mort generating $1,000,000 in net revenue, in the end his business generated a paltry $37,500 after taxes. He simply couldn't control his costs or charge what he needed to charge to earn a healthy margin.

Arthur's Return on Tangible Assets was 18%. Mort's...7.5%.

Arthur also made a lot more money despite equal sales and equal assets.

In short, you'd rather own Arthur's Bakery because it's a better business. It generates more cash for its owners, all things (assets) being equal.

And let's not forget Mr. Buffett's addendum:

The very best businesses are the ones that earn a high rate of return on tangible assets and grow.

What does growth have to do with it?

As investors, we want the companies we own to grow revenue, widen margins, and ultimately generate more cash for the owners (that’s us!).

Let's look at what happens if we factor in growth.

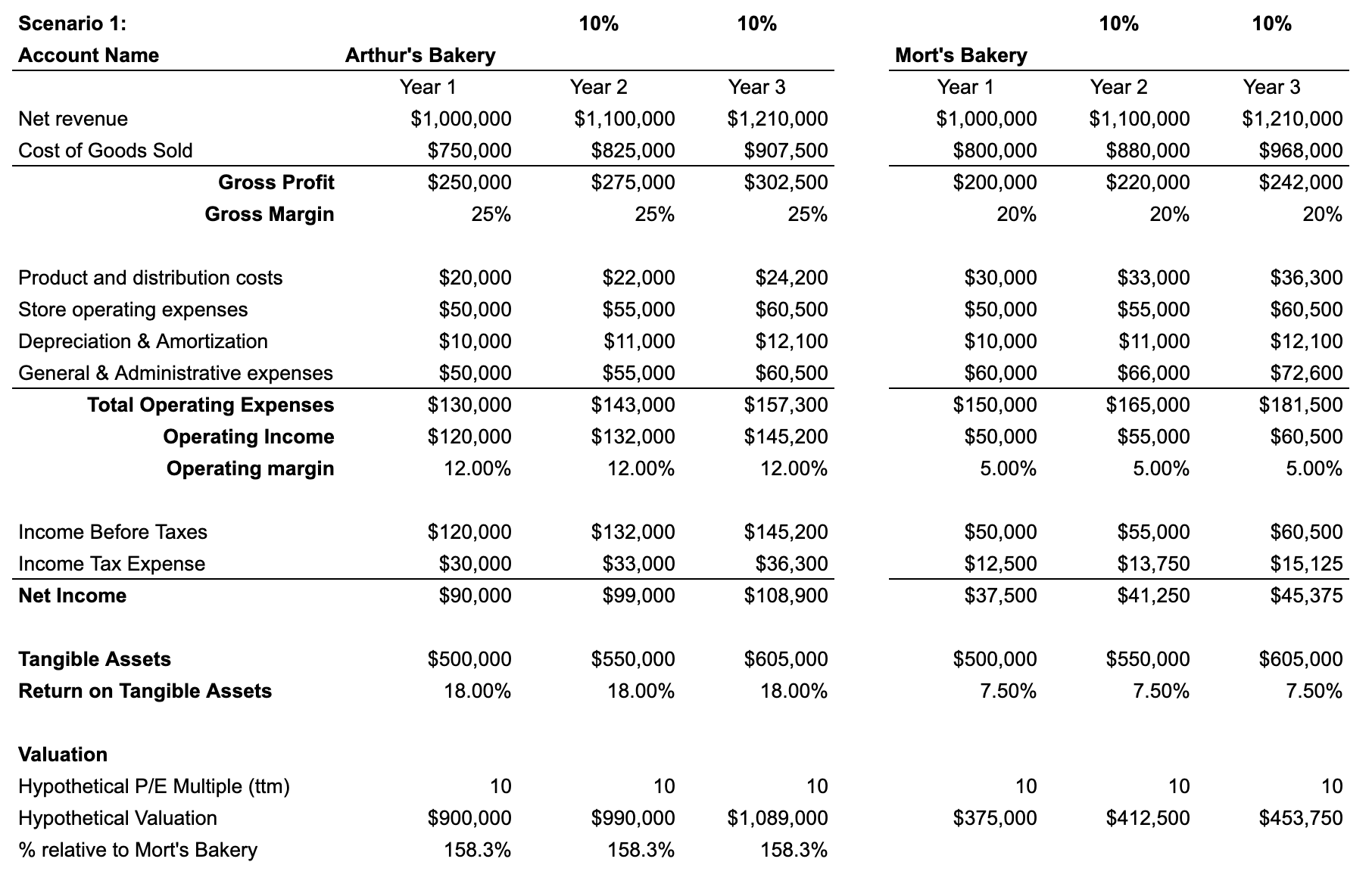

Scenario 1: Both bakeries grow 10% per year

Let's assume both bakeries grow at 10% per year after year one. Their valuations move in lock step with their growth rates.

Assuming the market will pay 10x earnings for each business, Arthur's Bakery is worth quite a bit more.

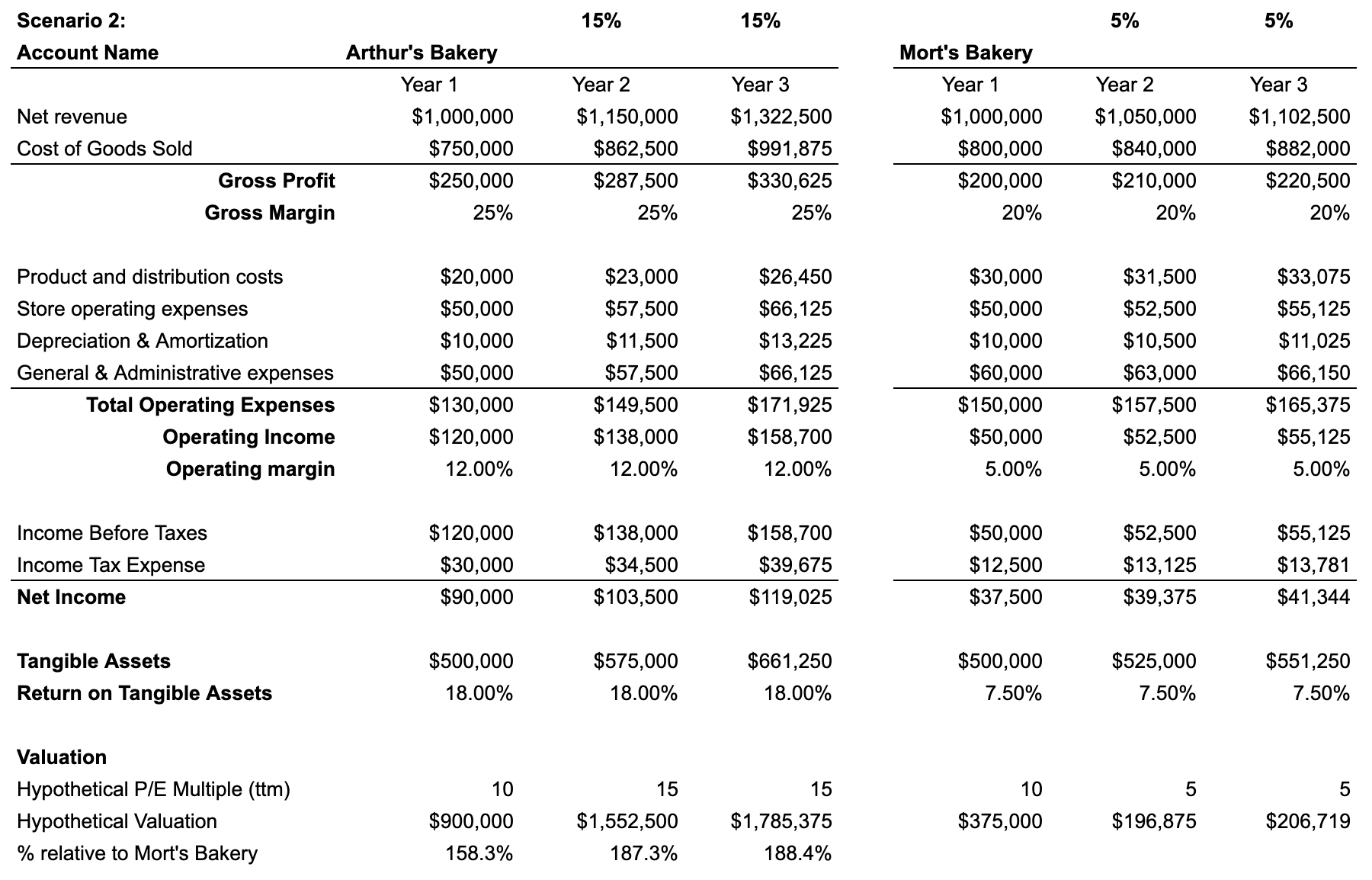

Scenario 2: Arthur's grows 15% per year. Mort's...only 5% per year

A more realistic scenario is one where Arthur's business grows faster than Mort's thanks to his competitive advantages.

Here, we'll not only assume different growth levels, but we'll also begin to reflect the market's natural tendency to place a premium on businesses that grow faster than their peers.

If the multiples are adjusted for the growth rates of the business, the 'how much is this business worth' gap between Arthur's Bakery and Mort's Bakery begins to widen: from 158% premium to 188% in just three years.

This widening will accelerate over time thanks to compounding.

Tying it all together

A company that is able to generate a higher return on assets is a good business.

A company that can continue to do that and grow is a great business.

Great businesses are rare. And it isn't as easy as screening for companies with high Return on Tangible Assets and just picking from the top. What matters is the future of the business.

...when we find [a good] business we try to figure out whether the economics of it means the earning power over the next five, or 10, or 15 years is likely to be good and getting better or poor and getting worse.

Warren Buffett

Good and getting better. I like that phrase.

It's not always obvious what factors for any given company will ultimately lead to growth or decline. But that's our job as investors – to identify the factors that matter and ignore the noise.

If you find a good business whose economic future is all but certain to improve, you may have found a great business.

Pay a reasonable price, and you may have found a great investment.